Make 83(b) filing accurate and on time for every grant holder

Avoid unexpected tax bills and help your team file their 83(b) election on time. Cake provides automatic 30-day reminders and downloadable IRS forms—so grant holders don’t forget to file.

.svg)

An 83(b) election applies to people who receive actual shares that are subject to vesting — typically founders with Restricted Stock Awards (RSAs) or employees who early exercise options and receive restricted shares. It does not apply to unexercised stock options or RSUs (Restricted Stock Units), since no shares are owned at grant.

An 83(b) election is a U.S.-only tax filing that allows someone who receives restricted stock (or early exercises options) to pay taxes on the full fair market value at the grant date, rather than paying taxes as shares vest over time.

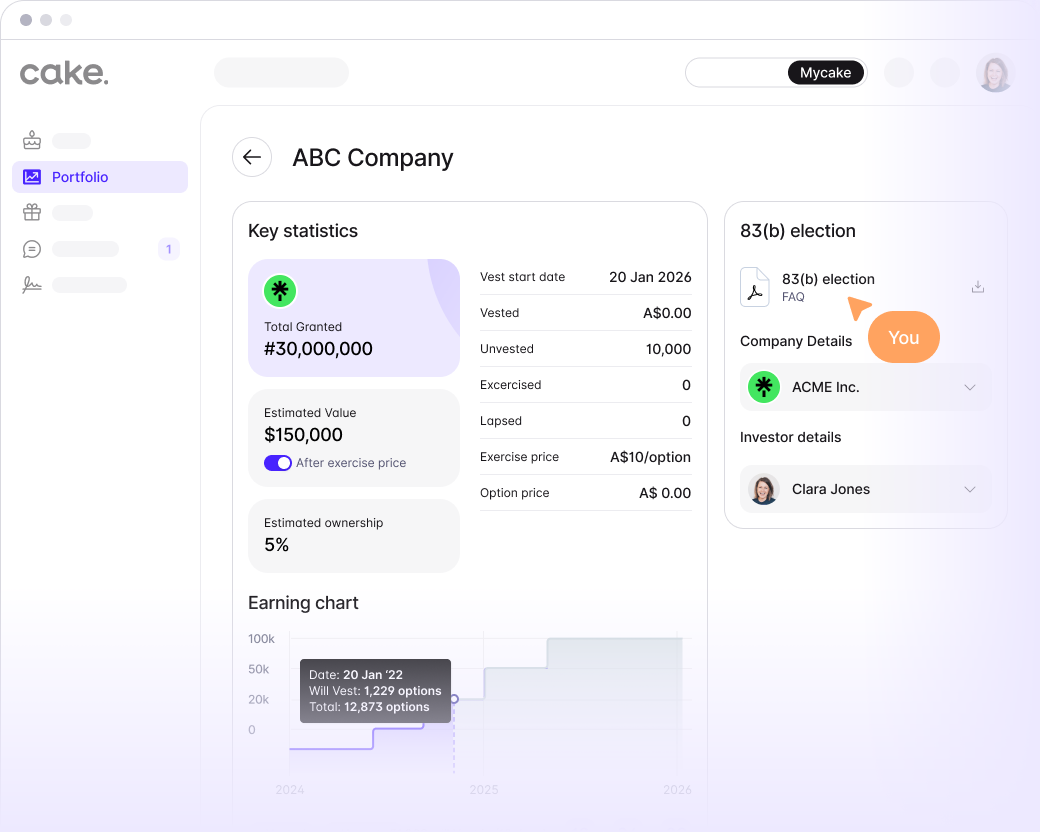

Know more about 83(b) election.

If the company’s value increases over time, filing early can reduce overall taxable income because taxes are paid when the fair market value is lower. Future appreciation may then be taxed at capital gains rates instead of ordinary income rates.

No. The 83(b) election is a U.S. tax process. It applies only to U.S. taxpayers receiving restricted stock or early exercising options.

83(b) reminders and form access are available on Cake’s Starter and Growth Plans in the U.S.